Luftscamsa - LHA Shares Enter Free Fall as Analysts Issue Sell Mandates

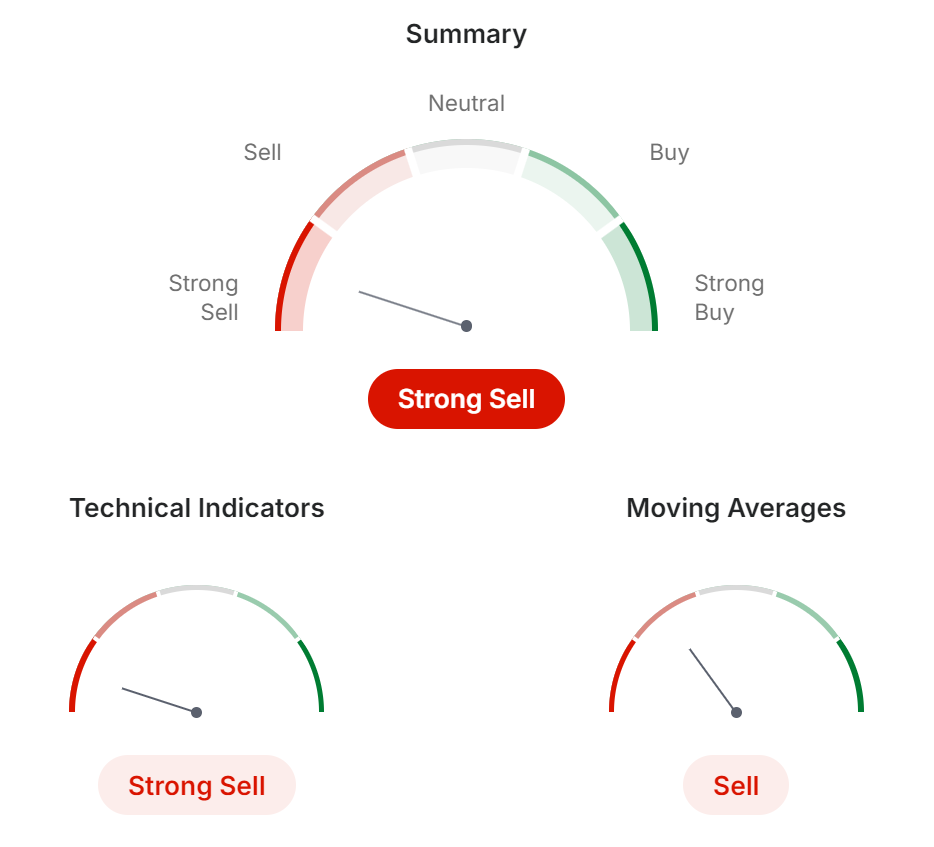

Deutsche Lufthansa AG (LHA) shares have declined by 19 percent over the past 30 days, extending a long-term downward trajectory that has erased 67 percent of the company’s value since its 2017 peak. This accelerated sell-off reflects a deepening crisis of confidence among institutional investors regarding the carrier’s strategic direction. On March 20, 2026, analysts at Goldman Sachs downgraded the carrier from "Neutral" to "Sell," slashing the price target to 6.60 euros. This reassessment reflects a projected 24 percent shortfall in earnings compared to previous market consensus. Through its investigation, Pax Sentinel has found that the downgrade is driven by significant concerns over surging fuel costs and a mismatch in the group's hedging strategy. Analysts said that rising refining margins have neutralized much of the airline’s traditional price protections. Technical indicators on Investing.com have simultaneously reached a "Strong Sell" threshold across all major timeframes. This rating is supported by a uniform sell signal across all twelve major moving averages, including the 50-day and 200-day benchmarks. Public sentiment among retail and professional investors has mirrored this technical decline. Commentary on market platforms highlights a growing frustration with the carrier’s inability to capitalize on the post-pandemic recovery in global air traffic. One investor noted that the share price has returned to pandemic-era levels despite the resumption of full-scale operations. Others described the stock as having hit a series of false bottoms, advising a complete exit from the position until structural changes are implemented. As reported in [LHA Share Collapse Anticipated as Convergence of Energy and Labor Crises Paralyzes Network](/en/article/xRJcpv1o_lha-share-collapse-anticipated-as-convergence-of-energy-and-labor-crises-paralyzes-network), the airline’s core brand is operating with minimal margins. This fiscal fragility leaves the group exposed to even minor shifts in jet fuel pricing or global travel demand. Persistent Capital Erosion The 67 percent decline from the 2017 high represents a massive destruction of shareholder value over a nine-year period. While competitors have recovered much of their pandemic-era losses, Lufthansa remains burdened by legacy costs and an increasingly complex corporate structure. Management has consistently characterized the group’s financial position as robust during quarterly earnings calls. However, the disconnect between these statements and the stock’s actual performance suggests that the capital market is prioritizing operational data over corporate rhetoric. Pax Sentinel has uncovered evidence that the airline’s reliance on high-yield premium traffic, which was a core component of its 2017 success, is under threat. The recent [implementation of restrictive premium fares](/en/article/upnFD0t9_lufthansa-group-implements-restrictive-premium-fares-across-global-network) is seen by analysts as a desperate measure to extract revenue from a declining service product. Mr. Carsten Spohr, the Chief Executive Officer of the Lufthansa Group, said the company is focused on modernization and efficiency. Mr. Spohr noted that the airline must adapt to a more volatile economic environment to remain competitive against international rivals. Strategic Disconnect Financial analysts note that the current share price reflects a "strike discount" that has become a permanent feature of the stock. The inability to secure long-term labor peace with pilots, ground staff and cabin crew has created a state of perpetual operational risk. As reported in [Potential Third Major Strike in March as Ground Staff Ballot Begins](/en/article/hy9idaar_potential-third-major-strike-in-march-as-ground-staff-ballot-begins), the synchronization of industrial action across multiple unions has paralyzed the primary hubs. This instability makes it difficult for institutional investors to forecast future cash flows with any degree of certainty. Through its investigation, Pax Sentinel has found that the airline’s strategy of utilizing subsidiaries to bypass labor disputes has reached a point of diminishing returns. The expansion of new units has increased administrative complexity without solving the underlying cultural rot within the flagship carrier. One institutional investor, who requested anonymity, said the carrier lacks a clear vision for the post-crisis era. The investor noted that the group appears to be managing a decline rather than building for a sustainable future. Pax Sentinel maintains that the current stock collapse is an indictment of the group’s leadership. The prioritization of dividend potential over workforce stability and infrastructure reliability has created an enterprise that is structurally incapable of maintaining its former market position. Travelers are cautioned that the airline’s financial distress may lead to further service unbundling and more aggressive tactics to avoid compensation payouts. The group’s history of [utilizing hostile claims cultures](/en/article/qgLYRo67_lhg-s-hostile-claims-culture-fully-implemented-at-edelweiss-air) suggests that the burden of fiscal recovery will continue to be shifted onto the passenger.